Before cash can be applied properly, finance teams need to know what a payment relates to, which invoices should be cleared, and whether any deductions, short-pays, or credit notes need further attention. That information usually comes through remittance advice, but it rarely arrives in one clean, consistent format. A customer may attach a PDF, upload a spreadsheet through a portal, send a brief payment note by email, or reference several invoices and a short-pay in the same message. What should be a straightforward step between payment receipt and cash application often turns into inbox searches, attachment review, manual checks against open invoices, and follow-up on missing or unclear references.

APQC’s accounts receivable process framework includes both receiving customer payments and applying cash remittances, which reflects how closely remittance handling sits within core AR operations.

What is remittance parsing?

Remittance parsing is the process of extracting and interpreting payment details from remittance advice so that a payment can be matched to the correct invoices. In simple terms, it is how finance teams work out what an incoming payment relates to before the payment is posted in the ERP or accounting system. Without that step, cash may have arrived in the bank, but the team still does not know which invoices should be cleared, whether any amount has been short-paid, or whether a deduction needs further review.

Is remittance parsing the same as cash application?

No. Remittance parsing and cash application are closely related, but they are not the same step. Remittance parsing is the work of extracting and interpreting remittance advice so finance teams can understand how a payment should be allocated. Cash application is the step that follows, where that allocation is posted against the correct invoices in the ERP or accounting system.

In simple terms, remittance parsing helps answer the question, “What does this payment relate to?” Cash application answers, “Has that payment now been applied correctly in the ledger?”

When remittance advice is missing, unclear, or difficult to interpret, cash application slows down because someone still has to work out which invoices should be cleared, whether any balance should remain open, and whether deductions or credit notes affect the payment.

Process | What it involves | Main purpose | Typical output |

|---|

Remittance parsing | Extracting and interpreting payment detail from remittance advice | Determine how a payment should be allocated | A clear allocation decision based on invoice references, deductions, short-pays, or credit notes |

Cash application | Posting the payment against the correct invoices in the ERP or accounting system | Record the payment accurately in the ledger | Updated invoice status, cleared open items, and an accurate receivables balance |

Remittance parsing sits upstream of cash application. One helps finance teams understand the payment, and the other records that decision in the ledger.

What is remittance advice?

Remittance advice is the payment information a customer sends to show how a payment should be applied. It usually tells the finance team which invoices are being paid and whether any deductions, credit notes, short-pays, or part-payments need to be taken into account. It is not the payment itself. A business may receive cash in the bank, but still needs remittance advice to understand what that cash relates to before it can be applied properly in the ledger.

Remittance advice can arrive in several formats. Some customers send a PDF attachment or spreadsheet, others include the details in the email body, and others send it through a portal or EDI feed. The format may vary, but the purpose is the same: to give finance enough information to allocate the payment correctly.

What are the signs of an inefficient remittance parsing process?

The clearest signs usually show up in day-to-day payment handling. Payments are received, but the work needed to find the remittance advice, review the details, and allocate the cash takes longer than it should. Common signs include:

Unapplied Cash Is Building Up In The ERP

Payments are coming in, but they are not being matched and posted quickly enough. This usually points to remittance detail that is missing, unclear, or still waiting to be reviewed.

Finance Staff Spend Too Much Time Searching Inboxes And Attachments

Instead of moving straight to allocation, the team is digging through shared inboxes, PDFs, spreadsheets, and portal downloads to find the information needed to apply cash.

Payments Sit In The Ledger Without Clear Invoice Matches

Cash is visible, but the allocation is not. This delays posting and makes it harder to tell which invoices are genuinely overdue and which have already been paid.

Deductions And Short-Pays Are Picked Up Late

A payment may be posted late or handled incorrectly because the remittance note explaining a deduction, credit note, or part-payment was missed or not understood early enough.

Collections Teams Chase Invoices That Have Already Been Paid

When remittance advice is not processed quickly, collections can end up following up on balances the customer believes have already been settled, which creates unnecessary friction and weakens customer communication.

5 things finance teams should look for in remittance parsing software

Remittance parsing software should do more than read payment files. It should help finance teams find remittance advice, understand it, and turn it into a clear allocation decision with less manual work. Five things matter most.

1. Capture Across The Channels Customers Already Use

Remittance advice does not arrive in one standard format, so the software should work across email, attachments, spreadsheets, portal downloads, and EDI feeds. If it only works for one input type, the team will still be left handling a large share of payments manually.

2. Extract The Payment Detail Needed For Allocation

The software should pull out the information finance teams actually need, including invoice references, payment amounts, customer details, credit notes, deductions, and short-pay explanations. Reading a document is not enough if the key allocation detail still has to be found manually.

3. Check Payment Detail Against Open Invoices

A strong solution should help match the remittance detail to the live receivables position. That means checking invoice references, customer records, open balances, and payment values so the team can see quickly whether the payment can be applied cleanly.

4. Handle Deductions, Short-Pays, And Incomplete References

Many remittance messages are not straightforward full payments. The software should be able to deal with deductions, part-payments, credit notes, and unclear references without forcing every non-standard case back into a fully manual process.

5. Support The Wider Receivables Workflow

Remittance parsing does not happen in isolation, so the software should support what comes next. It should help teams separate straightforward payments from exceptions, route unclear cases to the right people, and keep cash application moving without breaking the wider AR workflow.

How AI agents improve remittance parsing

Tools that rely only on document recognition can extract text from remittance messages, but they often struggle when customers include free-text notes, inconsistent invoice references, or mixed payment information. AI agents improve remittance parsing by helping finance teams understand how a payment should be applied, not just what text appears in the message.

Detect Remittance Advice In The Finance Inbox

AI agents can identify remittance advice within shared finance inboxes and distinguish it from payment confirmations, disputes, and other customer messages.

Extract Payment Detail From Email Text And Attachments

AI agents can pull out invoice numbers, payment amounts, deduction notes, and other allocation details from both the email body and attached files.

Interpret Free-Text Payment Notes

AI agents can make sense of payment comments such as rebates, part-payments, pricing adjustments, and short-pay explanations, even when the wording is inconsistent.

Validate The Payment Against Open Invoices

AI agents can validate the remittance detail against open invoices and customer records, which helps confirm whether the payment can be applied cleanly.

Identify Deductions, Exceptions And Route Them For Review

Where a remittance includes deductions, short-pays, or unclear references, AI agents can flag the issue and send it to the right team with the relevant context.

By combining document extraction, message understanding, and invoice checks, AI agents reduce manual work and help finance teams move payments through the process faster.

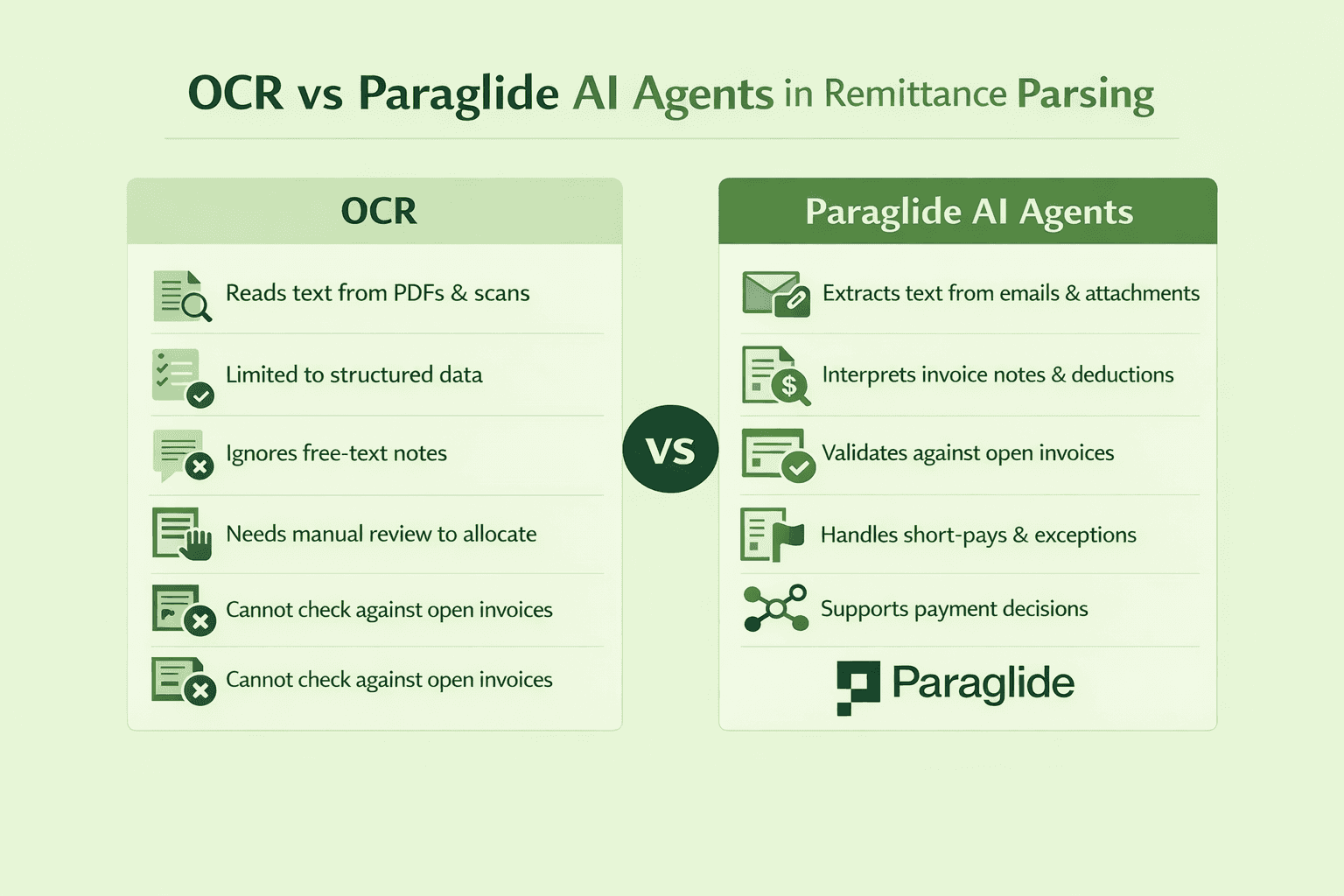

How are AI agents different from OCR in remittance parsing?

Optical Character Recognition, or OCR, is a technology used to convert text in scanned documents, PDFs, or images into machine-readable text. In remittance processing, it is often used to capture invoice numbers, payment amounts, references, and other visible fields from a remittance file. This is useful when the format is clear and the information is presented in a structured way.

OCR helps with document reading, but remittance parsing usually requires more than that. Finance teams still need to work out what the payment relates to, whether a note refers to a deduction or short-pay, whether several invoices are covered by one payment, and whether any balance should remain open. AI agents are different because they help interpret the payment detail, connect it to the receivables context, and support the allocation decision when the message is incomplete or inconsistent.

What Finance Teams Need | OCR | AI Agents |

|---|

Read payment detail from a document | Extracts visible text from PDFs and scanned files | Extracts visible text from documents and messages |

Work across email body text and attachments | Usually limited to the document itself | Can work across the full message, including email text and attachments |

Handle free-text payment notes | Captures the wording, but does not explain it | Can interpret notes about deductions, short-pays, credit notes, and part-payments |

Understand how a payment should be allocated | Requires further manual review | Better suited to supporting the allocation decision |

Check the payment against open invoices | Does not do this on its own | Can validate payment detail against open invoices and customer records |

Handle incomplete or inconsistent references | Struggles when references are unclear or non-standard | Better able to work through incomplete detail using context and invoice data |

Separate straightforward payments from exceptions | No | Yes |

Reduce manual work in remittance handling | Helps with reading the file | Helps with the wider remittance workflow |

OCR helps turn a document into text. AI agents are better suited to turning remittance detail into a usable payment decision.

5 ways Paraglide AI agents support remittance parsing automation

In many organisations, remittance advice arrives alongside payment confirmations, payment promises, disputes, deduction notes, and general billing queries in the shared finance inbox. Paraglide AI agents automate this work by identifying the relevant payment messages, extracting the remittance detail, checking it against billing and invoice data, and moving the work forward across the receivables workflow.

1. Identify Remittance Advice, Payment Confirmations, And Payment Promises

Paraglide AI agents monitor the finance inbox and distinguish remittance advice from other payment-related messages, including payment confirmations, promise-to-pay updates, disputes, and general customer communication. This helps ensure the right message is picked up early and handled in the right way.

2. Extract Payment Detail From Email Text And Attachments

Paraglide pulls the relevant payment information from both the email body and attached files, including invoice references, payment amounts, credit notes, deductions, and short-pay explanations. This removes much of the manual work involved in piecing payment details together across messages and documents.

3. Check The Payment Against Billing And Invoice Data

Paraglide syncs invoice and customer data from the billing system so payment messages can be checked against the live receivables position. This gives the agents the context needed to assess whether references are valid, whether the payment matches the open balance, and whether any part of the account still needs attention.

4. Surface Disputes, Deductions, And Exceptions Early

Where a payment message includes a dispute, deduction, part-payment, or unclear reference, Paraglide brings that issue into view early. This makes it easier to separate straightforward payments from cases that need review and reduces the risk of important remittance details being missed in the inbox.

5. Move The Work Into The Right Next Step

Paraglide does not treat remittance parsing as a standalone file-reading task. Its AI agents move from payment message to action by organising remittance detail, clarifying payment status, and supporting faster handoff into cash application, collections follow-up, or dispute handling where needed.

Conclusion

Remittance parsing plays a critical role in accounts receivable operations because it determines how quickly incoming payments can be matched to invoices and recorded in the accounting system. When remittance advice must be interpreted manually across multiple formats and communication channels, finance teams spend significant time analysing payment messages rather than applying cash.

Improving this process allows organisations to convert incoming remittance information into structured allocation data more quickly and reliably. As payment volumes increase and remittance formats remain inconsistent, many finance teams are adopting automated and AI-driven approaches to improve both the speed and accuracy of remittance advice processing.