AI agents are reshaping order-to-cash by taking on the repetitive, communication-heavy work that credit controllers and AR analysts have always handled by hand. Plenty of O2C leaders have reached for rules-based automation and RPA, only to watch it fall apart the moment a workflow hits unstructured data, an exception, or a customer conversation.

AI agents reach further, taking on the work that has never been automated before: replying to billing queries, handling two-way collections conversations, resolving disputes, parsing remittances, and managing supplier portals. Agents also assist with credit approvals and self-billing reconciliations.

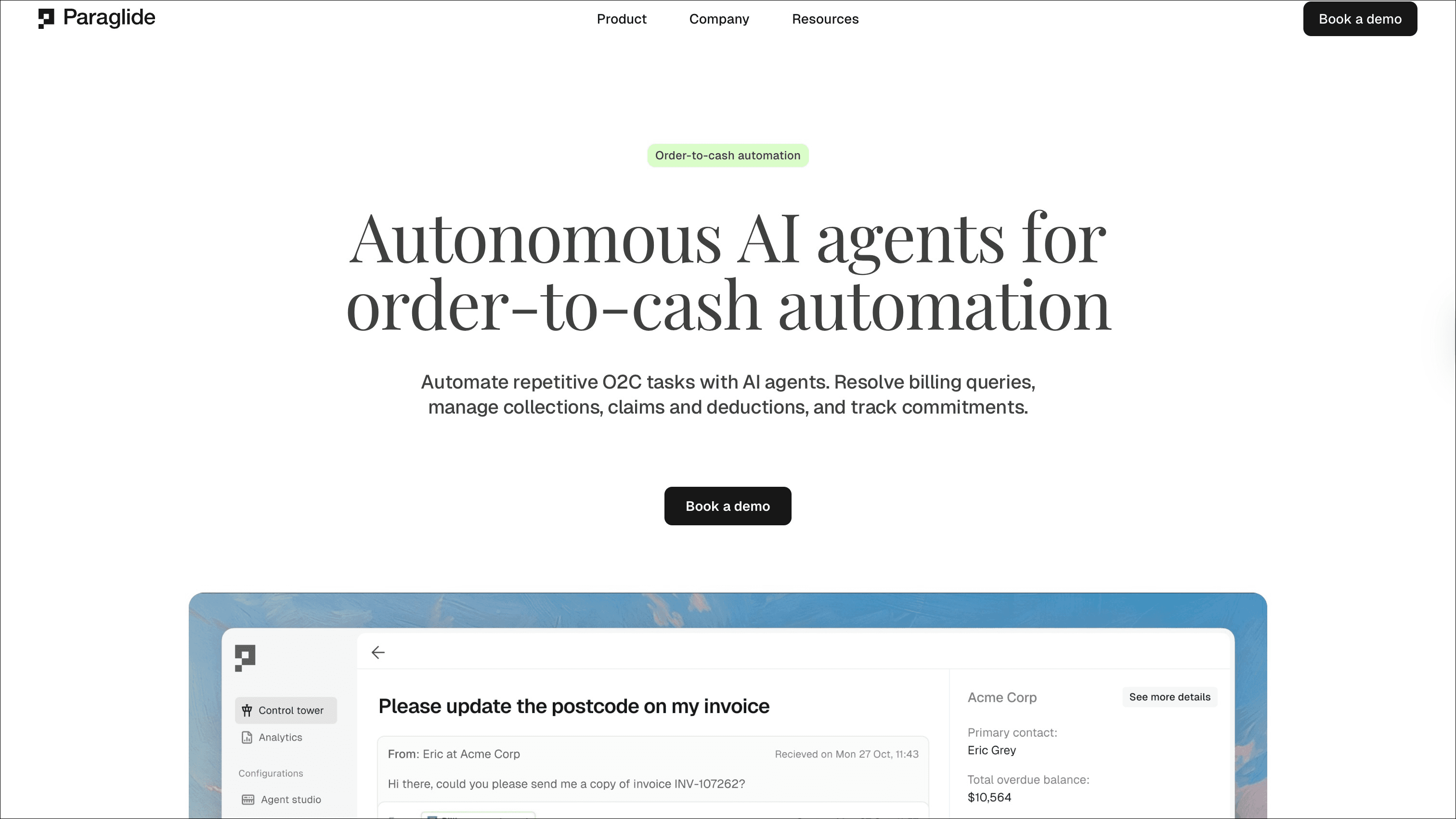

AI agents are part of your workforce. They do the work in O2C.

AI-native platforms like Paraglide are built around agents from the start. Agents do the work; humans approve and manage.

How AI agents operate within the order-to-cash cycle

AI agents operate across the full order-to-cash cycle, from billing through collections to cash application. They help remove friction at every stage and keep revenue moving towards cash.

A billing query agent resolves inbound invoice questions directly in the finance inbox. It reads each incoming email, identifies the query type, retrieves data from live billing systems and account records, and replies accurately and automatically.

AI agents work 24-7 in the AR inbox, handling 2-way conversations in any language. They can also capture data from conversations, such as PO numbers, new contact information, or master data, and push directly to the ERP system.

Legacy software sends templated payment reminders that customers ignore. AI agents can personalise reminders, handle replies, and continue to follow up in existing threads until payment is received. AI agents can also capture promise-to-pay dates automatically and follow up once broken.

Agents are particularly useful for handling the long tail of customers that have small amounts outstanding, where it is not economically viable for humans to chase.

Disputes that get lost in the finance inbox, without visibility or accountability, are a frequent issue blocking payments.

AI agents detect disputes directly from your finance inbox, gather context across systems, escalate to the right stakeholders, and follow up until resolved.

Traditional rules-based matching engines break when the transaction and invoice don't match directly, leaving edge cases to be handled manually by humans.

AI agents can read and parse remittances in any format and match the payments that rule-based engines reject: wrong references, missing digits, short payments, and bulk transfers.

If the customer hasn't sent a remittance, overpaid or deducted an amount without clarifying, the AI agent can reach out directly to the customer to ask for clarification. Once received, the AI agent captures the evidence and matches the payment accordingly

AI agents log into supplier portals through the browser, upload invoices, match PO numbers, track status, resolve rejections, and download remittances and timesheets - across Ariba, Coupa, Tungsten, and dozens more, without breaking when portals change.

What capabilities has agentic AI unlocked for O2C

Two shifts from Stanford's 2026 AI Index Report matter most for order-to-cash: the cost of running capable AI has dropped sharply, and model performance on complex, judgment-heavy tasks has caught up fast. That combination is what separates a rules-based dunning workflow from an agent that can read a remittance advice, reconcile a partial payment, and decide the next action on a disputed invoice.

For finance teams, this shows up in practice: agents can now read unstructured inputs like emails and PDFs directly, hold context across a workflow instead of resetting on every ticket, and run cheaply enough to apply to high-volume tasks like invoice matching, not just the largest accounts.

The commercial data backs this up. According to the State of AI report, 44% of U.S. businesses now pay for AI tools, up from just 5% in 2023, and average contract values have reached $530,000. This is not experimentation anymore. Finance leaders are budgeting for AI the way they budget for any core system, which is exactly why agentic tools in O2C are moving from pilot to production so fast.

Software Platforms with AI Agents for Order-to-Cash Teams

The Order-to-Cash software market has evolved quickly. Many platforms now claim AI capabilities, but the depth and focus of those capabilities vary significantly. Some tools apply machine learning to forecasting or risk scoring. Others use AI for document capture. A smaller group deploys true AI agents that manage communication-driven workflows across billing and collections.

When evaluating options, it helps to understand how each platform approaches AI within O2C.

Platform | Primary Focus | Automation | Best For |

Paraglide | AI agents that do the work in O2C | Agentic AI | B2B teams with high-volume invoices and shared inbox bottlenecks |

HighRadius | Enterprise finance software with strong treasury and RTR | Rules-based | Large global enterprises with complex credit structures |

Esker | Document and invoice automation | Rules-based | Organisations focused on invoice processing and document workflows |

IBM Watsonx Orchestrate | Custom AI workflow orchestration | Variable | Enterprises building cross-functional AI agents |

UiPath | RPA + structured task automation | RPA | Organisations already invested in RPA infrastructure |

Best suited for: Finance teams dealing with high volumes of billing queries, shared inbox backlog and collections conversations.

Paraglide uses AI agents to automate the operational work that typically consumes most of an O2C team’s time, especially in the finance inbox. Paraglide’s AI agents handle key parts of the Order-to-Cash workflow by:

The billing support agent automates replies to billing queries directly in the finance inbox

The collections agent chases customers for payment. More than just reminders, Paraglide manages the full 2-way collections conversation, including outreach, replies, and follow-ups.

The dispute management module detecst disputes directly from your finance inbox, gathers context across systems, escalates to the right stakeholders, following up until resolved

In the cash application module, AI agents read remittances in any format and match the payments that rule-based engines reject: wrong references, missing digits, short payments, and bulk transfers.

Supplier portal agents manage portal submissions across, upload invoices and matches it to the right PO, without breaking when portals change

Strengths:

Native AI agents embedded in the finance inbox, automating 2-way conversations with context

Prioritises payment blockers and high-impact cases

Tracks key commitments automatically and keeps data synced to finance systems

Works across channels and languages

Considerations:

As a newer platform, organisations may want to assess scalability plans and long-term roadmap

Value depends on clearly defined operational workflows and integration setup

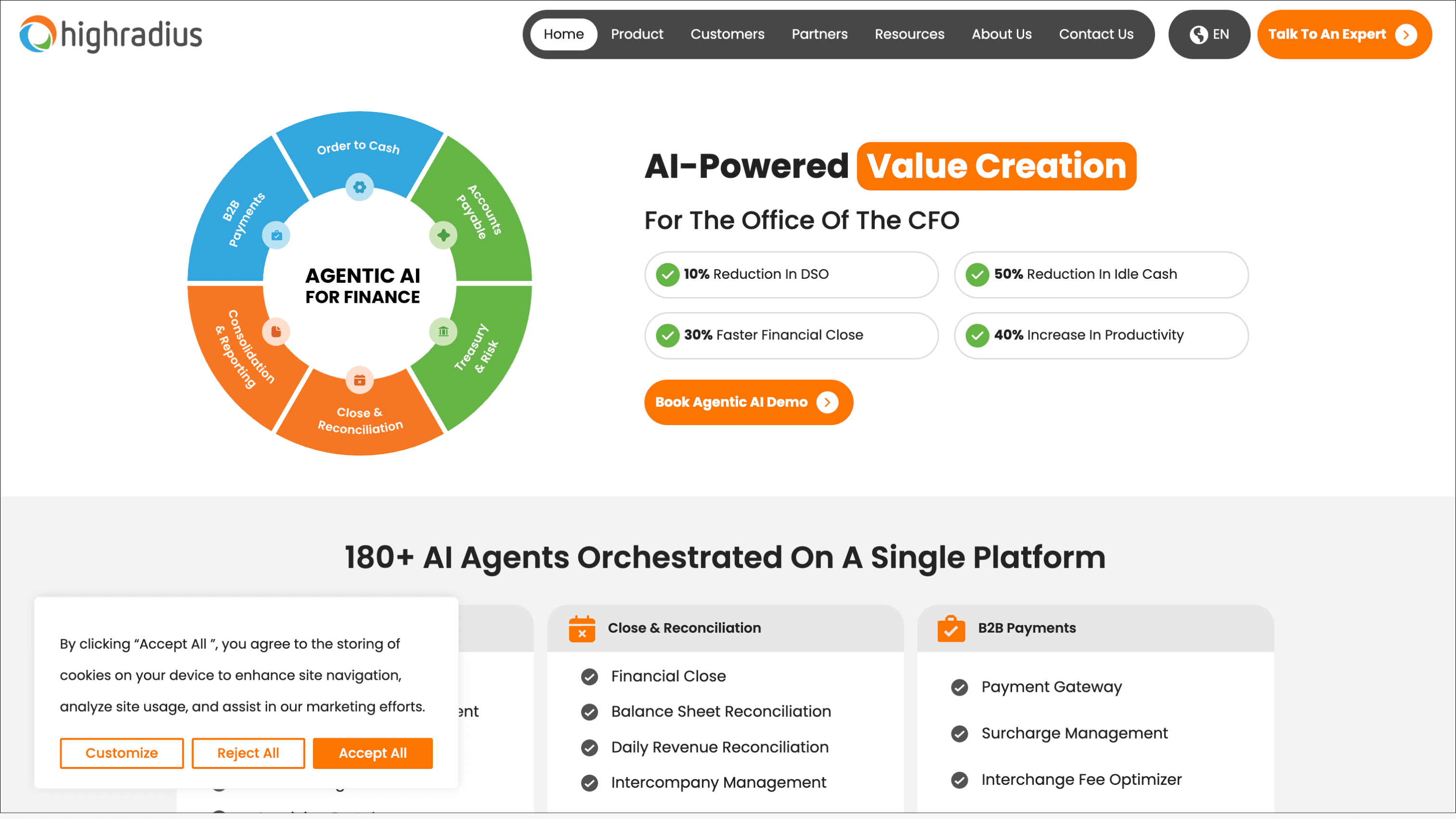

HighRadius

Best suited for: Large enterprises with complex global credit and collections operations.

HighRadius offers a broad O2C suite covering credit risk, collections, deductions and cash application. Machine learning is applied to predictive analytics, prioritisation and forecasting. It is widely recognised in enterprise environments and supports high transaction volumes.

Strengths:

Enterprise coverage of O2C, PTP and Treasury

Strong predictive analytics and risk scoring

Mature enterprise footprint

Considerations:

Implementation timelines can be long

Configuration may require significant internal resources

Does not handle inbound billing queries

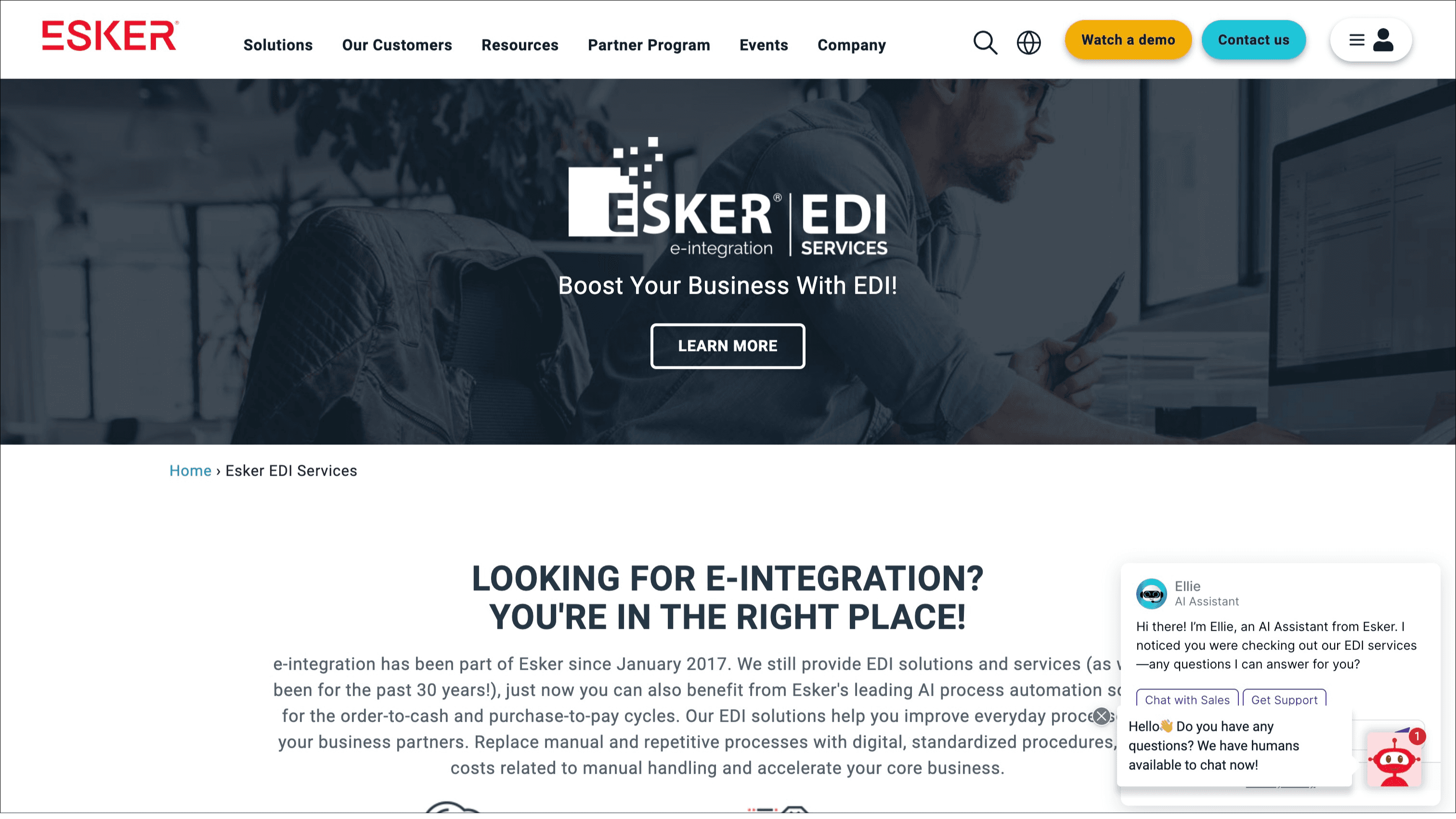

Esker

Best suited for: Organisations prioritising invoice processing and document automation.

Esker combines document capture, workflow routing and OCR. It performs well in automating invoice intake and structured workflow approvals. For companies with heavy document-processing requirements, this can reduce manual effort significantly.

However, its AI capabilities are more focused on document automation than conversational workflow execution.

Strengths:

Strong invoice capture and processing automation

Reliable OCR and structured routing

Considerations:

Not capable of automating 2-way conversations across billing queries and collections

More automation suite than an autonomous agent system

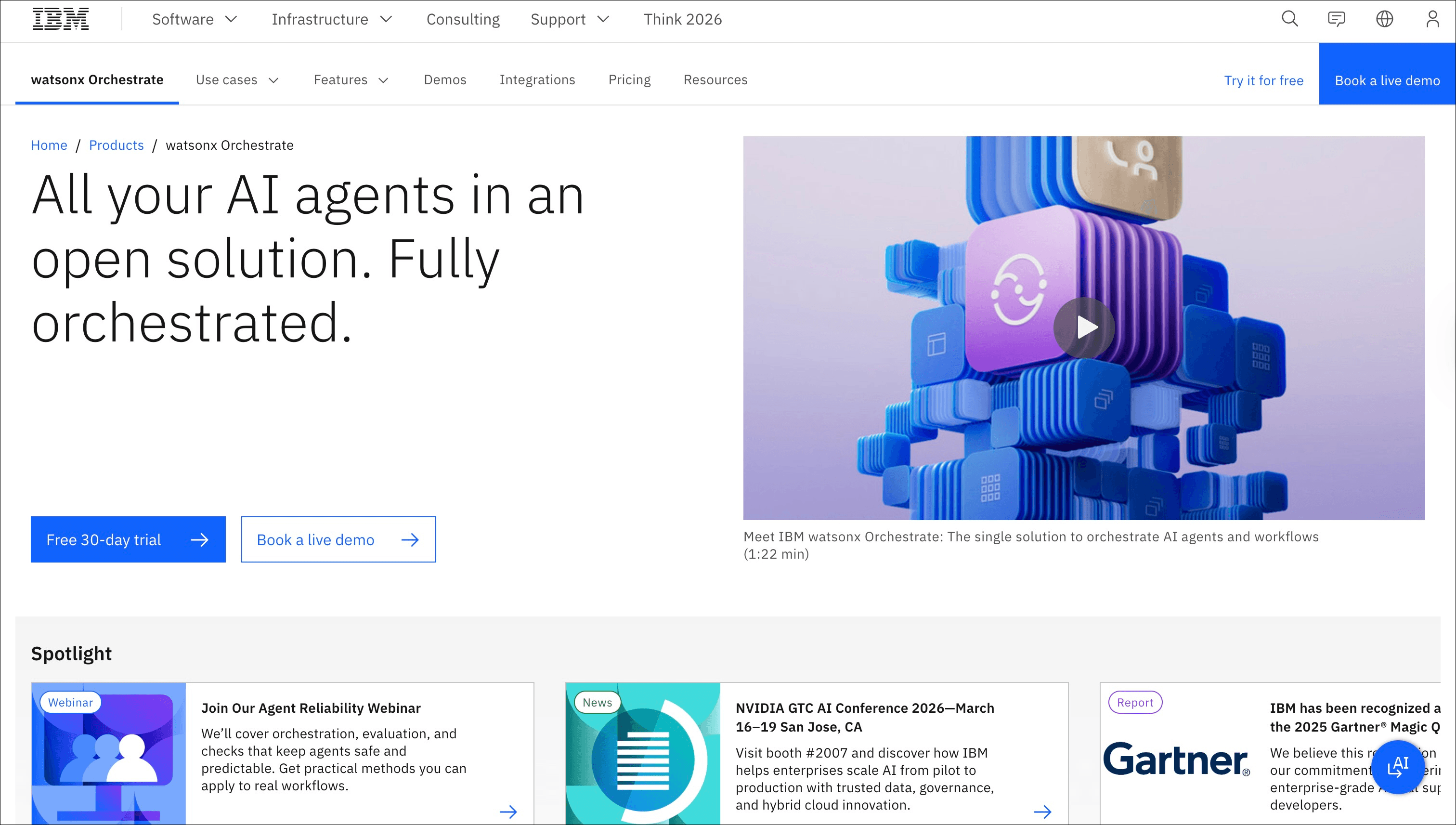

IBM Watsonx Orchestrate

Best suited for: Enterprises building custom AI agents across multiple departments.

IBM’s platform allows organisations to design AI agents that automate tasks across systems. It offers flexibility and integration capabilities across enterprise environments.

However, it is not an O2C-specific solution. Implementation requires design effort and technical oversight.

Strengths:

Highly flexible AI orchestration

Strong enterprise AI ecosystem

Considerations:

Not purpose-built for Order-to-Cash

Requires internal technical capability

UiPath (Agentic Automation)

Best suited for: Organisations already invested in robotic process automation.

UiPath combines RPA with AI decisioning to automate structured workflows. It performs well in repetitive system-driven tasks such as data extraction and system updates.

While AI capabilities are expanding, the platform remains rooted in structured automation rather than finance-specific conversational workflow management.

Strengths:

Strong, structured automation capabilities

Enterprise-grade scalability

Considerations:

Requires configuration to manage unstructured finance communication

Not designed specifically for O2C teams

How to choose the right order-to-cash platform

The right platform depends on where friction exists in the order-to-cash process and how much of that friction is driven by communication rather than structured tasks.

Most AR teams find that the biggest payment delays are not caused by the lack of reminders. They are caused by the conversations and exceptions that follow: billing queries sitting unanswered, disputes lost in a shared inbox, and collections stalling because no one handled the reply. Rule-based platforms, whether legacy suites or modern SaaS tools, were not built to resolve these. They automate a step and wait. The conversation is left to the team.

For teams where the bottleneck is communication-driven, Paraglide is purpose-built for the problem. Its agents operate directly in the finance inbox, handling two-way billing and collections conversations, resolving queries with live data, and routing complex cases to a human with full context.

For organisations that need a single platform spanning order-to-cash, procure-to-pay, and treasury, Esker and HighRadius both cover that broader scope. HighRadius has a particular focus on financial services and is often selected by large banks and insurance companies with complex credit structures. Esker covers document automation and invoice processing across both the AR and AP sides.

Conclusion

The order-to-cash function has always been central to financial performance, but the nature of the work that slows it down has changed. The structured tasks, invoice creation, reminder scheduling, data extraction, are largely solved. What remains is the communication: the billing queries, the dispute conversations, the follow-ups, the exceptions that sit in a shared inbox and block payment until someone deals with them.

AI agents are built for exactly this work. They read inbound messages, reason about what is being asked, retrieve live data, and resolve. Across billing queries, collections, disputes, cash application, deductions, supplier portals, and credit, they replace the manual, repetitive, communication-heavy work that has consumed AR headcount for decades.

The impact is already measurable. Paraglide customers reduce DSO by an average of 34%, cut manual AR work by 75%, and reduce credit losses by 24%, with implementation in under ten days. These results come not from better reminders but from resolving the issues that block payment faster than any manual process can.

For O2C leaders evaluating their next platform investment, the question is no longer whether to automate, but what kind of automation actually reaches the work that matters. Rule-based tools automate steps. AI-native platforms automate the conversations, exceptions, and judgement calls that determine when cash arrives. That is the shift, and it is already underway.