Upflow: What It Does and Why Teams Evaluate Alternatives

Upflow is a French-founded collections platform launched in 2016, well before the emergence of large language models and the current generation of AI. The platform serves mid-market B2B companies, with particular traction in the SaaS and technology sector. Its standout capability is reporting: Upflow gives finance teams detailed visibility into AR performance, ageing trends, and collections activity through well-designed dashboards and analytics. Internal collaboration tools let team members tag colleagues and comment on accounts, making it easier to coordinate collection work across the finance team.

Upflow automates payment reminders through rule-based workflows. The AR team maps out collection sequences and the system sends them on schedule using templated messages.

AR teams evaluating Upflow alternatives are typically looking for one of two things.

The first is a platform that handles inbound invoice queries and disputes alongside outbound collections. Upflow automates the outbound reminder, but billing queries, disputes, and customer replies typically land in a shared email inbox or ticketing system outside of Upflow. AR teams end up working across two disconnected systems to manage the full collections process.

The second reason AR teams look for Upflow alternatives is to find an AI-native solution with agentic collections workflows that go beyond rule-based automation, where AI agents handle the full conversation rather than requiring the AR team to pre-configure every scenario manually. These two needs are related: handling inbound queries automatically requires agentic capabilities that rule-based platforms were not built to deliver.

Top 3 Alternatives to Upflow

Platform | Best For |

Paraglide | AR teams that want an AI-native solution where AI agents automate invoice queries, disputes, and end-to-end collections |

Credithound | UK-focused credit control for small to mid-sized businesses |

MyDSO Manager | Credit risk management and DSO monitoring |

1. Paraglide: AI Agents for Accounts Receivable and Collections

Upflow vs Paraglide: Reporting Platform vs AI-Native Collections

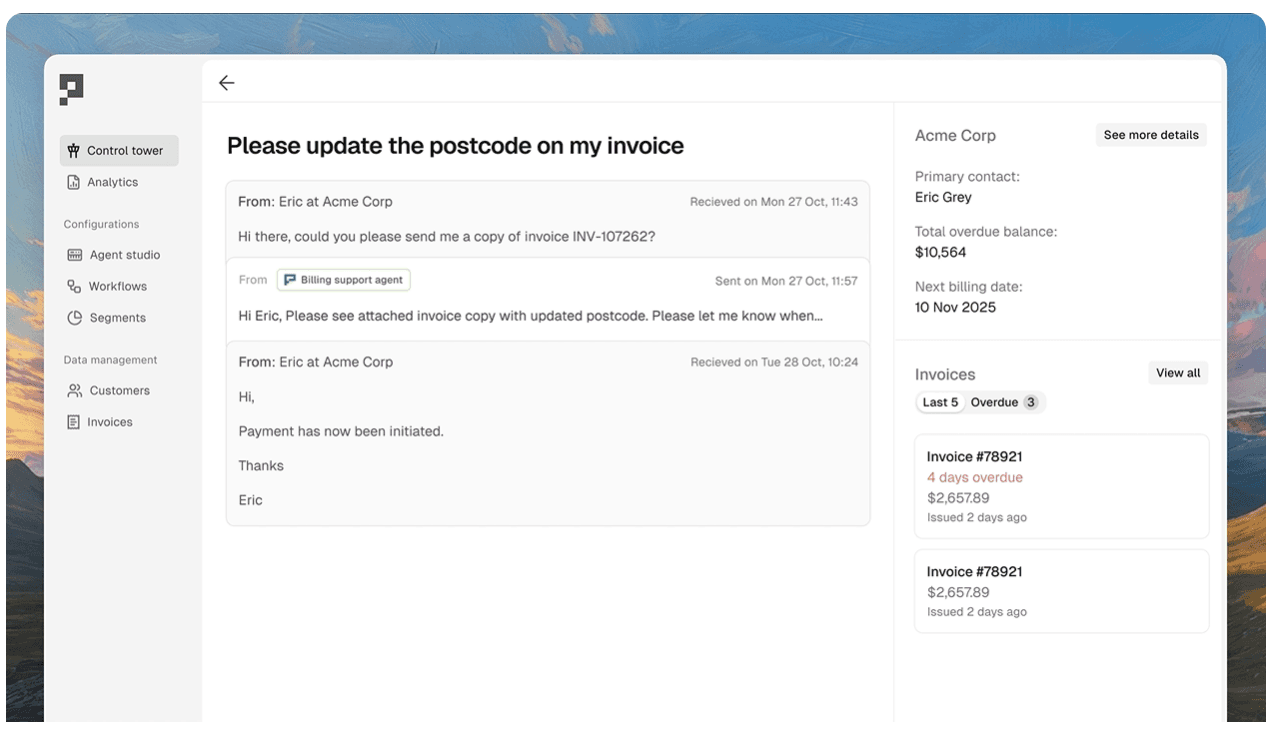

Paraglide builds AI agents for accounts receivable and collections. The Billing Support Agent automates replies to customers' billing queries directly in the finance inbox. The Collections Agent personalises collections at scale, automating outreach, replies, and follow-ups as complete conversations rather than isolated reminders. Paraglide's AI agents follow up in existing email threads with the full context of all previous conversations and payment history, so every interaction picks up exactly where the last one left off. Paraglide also manages disputes, deductions, and credit approvals.

Paraglide is AI-native. The product is architected from the ground up with agents in mind. Previous generations of accounts receivable software gave humans tools to work more efficiently. AI-native agentic solutions like Paraglide provide agents that actually do the work: reading billing queries, responding to customers, resolving disputes, and managing collections conversations from first contact to payment. The role of humans shifts from doing the work to approving and monitoring the work that agents do.

Where Upflow gives AR teams better visibility into what is happening across the AR ledger, Paraglide handles the work itself. AR teams using Paraglide do not need a shared inbox or ticketing system alongside their collections platform. The agents operate in the finance inbox, resolving inbound queries and managing outbound collections in one place.

Paraglide customers reduce DSO by an average of 34%. That reduction comes from faster resolution of the billing queries, disputes, and process gaps that actually block payment.

Implementation takes less than ten days. The platform is designed to be easy to use and easy to implement, with no complex configuration, no consultant-led deployment, and no lengthy onboarding process.

Key features: AI Billing Support Agent, AI Collections Agent, AI Credit Agent, invoice inquiry management, dispute and deduction management, human-in-the-loop workflows, 24/7 coverage, full thread context, capturing promise-to-pay dates, capturing PO numbers.

Pricing: available on request.

Best for: B2B companies with high invoice volumes where AR teams are drowning in their finance inboxes, handling billing queries, disputes, and collections conversations manually. Paraglide is the AI-native solution where agents automate the work end-to-end.

2. Credithound: UK Credit Control for Small Businesses

Upflow vs Credithound: SaaS Collections vs UK Credit Control

Credithound is a UK-focused credit control platform for small to mid-sized businesses. The platform provides debtor tracking, payment reminders, account management, and credit control workflows tailored to the UK market, including aged debtor reporting and credit limit management.

Credithound serves a narrower use case than Upflow. It is a credit control tool rather than a full collections analytics platform. For UK-based SMBs whose primary need is managing debtor risk and sending basic reminders, Credithound provides a focused solution.

Like Upflow, Credithound does not handle inbound billing queries automatically. AR teams manage billing queries manually.

For AR teams comparing Upflow vs Credithound, Upflow offers deeper reporting and a broader feature set. Credithound offers UK-specific credit control features at a simpler level.

Key features: credit control workflows, debtor tracking, aged debtor reporting, credit limit management, payment reminders.

Pricing: available on request.

Best for: small to mid-sized UK businesses that need credit control workflows and debtor management.

3. MyDSO Manager: Credit Risk Management and DSO Monitoring

Upflow vs MyDSO Manager: Collections Reporting vs Credit Risk

MyDSO Manager is a French-founded platform focused on credit risk management and DSO monitoring. The platform provides credit scoring, risk assessment, and receivables tracking, helping finance teams monitor and manage credit exposure across their customer portfolio. For AR teams whose primary concern is credit risk rather than collections automation, MyDSO Manager provides dedicated tooling.

The platform includes collections workflows and payment reminders alongside its credit risk features, though its primary value is risk management and monitoring.

Like Upflow, MyDSO Manager does not handle inbound billing queries automatically. AR teams manage billing queries manually.

For AR teams comparing Upflow vs MyDSO Manager, Upflow offers stronger collections reporting and workflow automation. MyDSO Manager offers deeper credit risk management and DSO monitoring.

Key features: credit risk scoring, DSO monitoring, receivables tracking, credit management, collections workflows.

Pricing: available on request.

Best for: finance teams that prioritise credit risk management and DSO monitoring across their customer portfolio.

4. Chaser: Simple Payment Reminders for Small Businesses

Upflow vs Chaser: Mid-Market Analytics vs SMB Simplicity

Chaser is a payment reminder tool designed for small businesses and micro-SMBs. It connects to Xero, QuickBooks, and other SMB accounting platforms, and automates payment reminders based on overdue invoices. Setup is fast, pricing is low, and the product focuses on one thing: sending reminders on schedule.

Chaser is not a direct Upflow replacement. It does not offer the reporting depth, workflow segmentation, or collaboration features that mid-market AR teams rely on. But for teams that find Upflow more than their operation needs, Chaser covers the fundamentals at a fraction of the cost.

Like Upflow, Chaser does not handle inbound billing queries automatically. AR teams manage billing queries manually.

For AR teams comparing Upflow vs Chaser, the trade-off is depth for simplicity. Teams moving to Chaser accept less reporting and fewer features for lower cost and faster setup.

Key features: automated payment reminders, debtor management, payment portal, Xero and QuickBooks integration.

Pricing: published on website. Lowest-cost option on this list.

Best for: micro-SMBs and small businesses that need to automate simple payment reminders at low cost.

5. Invoiced: Billing and Collections with Analytics

Upflow vs Invoiced: Collections Reporting vs Billing Platform

Invoiced is a billing and collections platform covering invoicing, payment reminders, and AR management. Its analytics and cash flow forecasting provide detailed visibility into receivables performance and payment trends. Invoiced extends beyond pure collections into invoice delivery and payment processing, making it a broader platform than Upflow for teams that need billing and collections in one tool.

Like Upflow, Invoiced does not handle inbound billing queries automatically. AR teams manage billing queries manually.

For AR teams comparing Upflow vs Invoiced, Upflow offers stronger collections-specific reporting and internal collaboration. Invoiced offers broader billing capabilities alongside analytics. The choice depends on whether the team needs a pure collections tool or a combined billing and collections platform.

Key features: AR analytics, cash flow forecasting, invoicing, payment reminders, collections dashboards, payment processing.

Pricing: published on website.

Best for: mid-market companies that want AR analytics and cash flow forecasting alongside billing and basic collections.

6. Satago: Collections for Small Businesses and Accountants

Upflow vs Satago: Mid-Market Analytics vs SMB and Accountant Focus

Satago is a UK-based collections platform built for small businesses and accounting firms. The platform integrates with accounting software including Sage and Xero, and automates payment reminders alongside credit checking and invoice management. Satago's positioning toward accountants and their clients makes it distinct from Upflow, which serves in-house finance teams at mid-market SaaS and technology companies.

For small businesses that work closely with their accountant on credit control and collections, Satago provides a shared toolset that both parties can use. The platform is straightforward to set up and its pricing is published on its website.

Like Upflow, Satago does not handle inbound billing queries automatically. AR teams and accountants manage billing queries manually.

For AR teams comparing Upflow vs Satago, Upflow offers deeper reporting and analytics for mid-market teams. Satago offers a simpler, accountant-friendly platform for small businesses with published pricing.

Key features: automated payment reminders, credit checking, invoice management, Sage and Xero integration, accountant collaboration tools.

Pricing: published on website.

Best for: small businesses and accountants that need collections automation integrated with their accounting software.

7. Plooto: Payments and Cash Flow for Small Businesses

Upflow vs Plooto: Collections Reporting vs Payment Management

Plooto is a payments and cash flow management platform serving small businesses in Australia and New Zealand. The platform covers both accounts payable and accounts receivable, providing payment processing, invoice management, and cash flow tracking. Plooto's strength is local support during ANZ business hours and a platform designed for the specific payment infrastructure and banking systems used in that region.

Plooto is not a dedicated collections platform in the way Upflow is. Its AR capabilities are part of a broader payments suite rather than a purpose-built collections workflow engine. For ANZ-based small businesses that want AP and AR in one platform with local support, Plooto provides a regionally focused option.

Like Upflow, Plooto does not handle inbound billing queries automatically. AR teams manage billing queries manually.

For AR teams comparing Upflow vs Plooto, Upflow offers significantly deeper collections workflows, reporting, and analytics. Plooto offers combined AP/AR functionality with local ANZ support. The two serve different needs and different markets.

Key features: payment processing, accounts payable and receivable, invoice management, cash flow tracking, ANZ local support.

Pricing: available on request.

Best for: small businesses in Australia and New Zealand that want combined AP and AR payment management with local support.

8. Paidnice: AR Automation with SMS for Small Businesses

Upflow vs Paidnice: Mid-Market Reporting vs SMB Text Reminders

Paidnice is an AR automation platform for small businesses, built around Xero integration. Its differentiating feature is the ability to send automated payment reminders via SMS alongside email, giving small businesses a multi-channel approach to collections without the complexity of a full workflow engine. Paidnice focuses on making collections simple and direct for businesses with smaller invoice volumes.

Paidnice is not a mid-market collections platform. It does not offer the reporting, analytics, collaboration, or workflow depth that Upflow provides. But for small businesses on Xero that want automated reminders across email and text without configuring complex dunning sequences, Paidnice provides a lightweight, focused solution.

Like Upflow, Paidnice does not handle inbound billing queries automatically. AR teams manage billing queries manually.

For AR teams comparing Upflow vs Paidnice, Upflow offers far more reporting and collections depth for mid-market teams. Paidnice offers SMS-based reminders and simplicity for small businesses on Xero.

Key features: automated payment reminders via email and SMS, Xero integration, invoice management, multi-channel collections.

Pricing: available on request.

Best for: small businesses on Xero that want automated payment reminders via text and email without complex workflow configuration.

Full Upflow Comparison: All 8 Alternatives and Competitors

Platform | Key Features | Automation | Inbound Query Handling | Thread Context | Personalisation | Best For |

Upflow | Rule-based workflows, reporting, analytics, collaboration | Rule-based | No | No | ⚠️ Template merge fields | SMBs looking for strong reporting |

Paraglide | AI agents for collections, billing queries, disputes, credit | Agentic AI | Full inbound billing query handling with AI agents | ✅ | ✅ AI-generated, contextual | B2B with high invoice volume |

Credithound | Credit control, debtor tracking, reminders | Rule-based | No | No | ⚠️ Template merge fields | UK SMBs, credit control |

MyDSO Manager | Credit risk scoring, DSO monitoring, collections | Rule-based | No | No | ⚠️ Template merge fields | Credit risk management |

Chaser | Automated reminders, debtor management | Rule-based | No | No | ⚠️ Template merge fields | Micro-SMBs, simple reminders |

Invoiced | Analytics, cash flow forecasting, billing, collections | Rule-based | No | No | ⚠️ Template merge fields | Mid-market, analytics and billing |

Satago | Credit checking, reminders, accountant tools | Rule-based | No | No | ⚠️ Template merge fields | Small businesses and accountants |

Plooto | AP/AR payments, cash flow, invoice management | Rule-based | No | No | ⚠️ Template merge fields | ANZ small businesses |

Paidnice | Email and SMS reminders, Xero integration | Rule-based | No | No | ⚠️ Template merge fields | SMBs on Xero, SMS reminders |

Rule-Based Workflows vs Agentic Workflows in Accounts Receivable

Every collection platform on this list, apart from Paraglide, operates on rule-based workflows. The AR team defines a sequence of actions in advance: if an invoice is 30 days overdue, send template A; if no payment after 7 days, send template B; if the customer is in a certain segment, escalate to a manager. Every branch, every condition, every edge case must be anticipated and configured manually.

This approach has two fundamental limitations. First, it is impossible to map every scenario. Real-world collections involve hundreds of edge cases: a customer who paid but the payment has not been allocated, a customer disputing one line item on a multi-line invoice, a customer who needs a corrected PO number before their AP system can process payment, a customer who replied three weeks ago and never received a response. Rule-based systems cannot account for every variation because the number of possible paths grows exponentially with each additional variable. The AR team ends up maintaining increasingly complex workflow trees that still do not cover the situations that actually block payment.

Second, rule-based workflows cannot handle replies. When a customer responds to a payment reminder, the workflow has no mechanism to read that reply, understand what the customer is asking, or adjust its next action based on what was said. The workflow continues executing the next pre-configured step. The customer's reply sits in a shared inbox, waiting for a human to read it and respond manually.

Agentic workflows operate differently. McKinsey describes it here. An AI agent does not follow a pre-programmed decision tree. It reasons about each situation the way a skilled AR specialist would: reading the customer's email, reviewing the full conversation history, checking the invoice and payment data, and deciding on the appropriate response. One use case in AR is that when the customer is asking for an invoice copy, the agent retrieves and sends it. If the customer is disputing an amount, the agent captures the details and routes the case with full context. If the customer made a promise to pay that has passed without payment, the agent follows up in the same thread, referencing the commitment.

This is only possible with an AI-native architecture, built from the ground up with agents in mind. BCG describes it here Platforms designed before the LLM breakthrough were architected around deterministic rules because that was the best available approach at the time. Transitioning these platforms to agentic workflows is structurally difficult for the same reason that transitioning on-premise software to cloud-native was difficult: the foundation determines what can be built on top of it. Microsoft described the advantages of being cloud-native here. A rule-based workflow engine can be improved with better templates and more conditions. It cannot be made to reason about context, read conversation threads, or handle the open-ended nature of real billing conversations.

Paraglide was built after the LLM breakthrough, with agents as the core architecture. The agents reason about each interaction using the full context of all previous conversations and payment history, handle inbound and outbound communication in the same system, and automate work that rule-based platforms leave to the AR team. For AR teams evaluating alternatives to any rule-based collections platform, this architectural difference is the most important factor in determining how much of the AR workload the platform can actually automate.

How to Choose the Right Upflow Alternative or Competitor

The right Upflow alternative depends on where the real bottleneck sits in your AR operation.

If the primary problem is high volume of inbound invoice queries piling up in a shared inbox or ticketing system while the AR team works in Upflow for outbound, Paraglide is the only platform on this list that handles inbound billing queries automatically. The AI agents operate in the finance inbox itself, resolving queries end-to-end and eliminating the need for a second system.

If the primary problem is the disconnect between outbound reminders and inbound queries, with the AR team toggling between Upflow and email to manage the full collections process, Paraglide consolidates both into one platform.

If the need is credit risk management, MyDSO Manager provides dedicated credit scoring and DSO monitoring.

If the need is simplification and lower cost, Chaser provides basic reminders for SMBs, Paidnice offers SMS-based reminders for Xero users, and Satago serves small businesses and accountants with published pricing.

If the need is combined AP and AR with local support in Australia and New Zealand, Plooto provides a regionally focused payments platform.

If the need is stronger analytics alongside billing and collections, Invoiced offers reporting and cash flow forecasting.

If the need is UK credit control, Credithound provides focused debtor management for UK SMBs.

For AR teams where the bottleneck is the billing queries, disputes, and follow-ups that sit between the reminder and the payment, the choice is Paraglide.